In October last year I got an email from Vanguard that they were wanting me combine my traditional Vanguard accounts which held Vanguard mutual funds with my Vanguard Brokerage Accounts which I used to buy and sell stocks and exchange traded funds. I had one account of each type for taxable investing and for Roth IRA’s. So I had four accounts and they wanted me to go to two accounts. Here is how they put it:

To make investing easier for you, we’re simplifying our account structure and we need your help . . . This change won’t cost you a thing, and it will help us serve you more efficiently. While we would like to make the switch for you, we need your permission to move your Vanguard mutual funds into brokerage accounts.

I’ve always liked Vanguard’s approach to investing and they have been pretty good to work with, so I made the move right away. Nothing in the email warned me of any possible problems, just that it would be easier, simpler, and more efficient. I made the change immediately.

As I got towards November, I had to pay my property taxes which went up 25% this year. I didn’t have the money in my checking account, so I needed to pull some from my short term bond fund at Vanguard. I waited until a couple of weeks before the taxes were due to order the transfer online. When I went to place the order I was told that my bank account was no longer connected to my Vanguard account. Before I had all four of my Vanguard accounts connected to my bank account, the same Bank of America checking account I have had for 25 years and that I have used routinely with Vanguard. That was weird, but I figured I could just re-enter the account number and routing information like I did originally back in the 1990’s. Nope. Instead I needed to print out some forms, fill them in, sign them, and mail them in to Vanguard so they could connect my investment account to my bank, a process that could take 2 weeks. I didn’t have 2 weeks. I called customer service. They said there was no way they could do this online even though I don’t think I have ever had to mail anything to any utility company or other financial company to do electronic debits in the past. And this was for a bank account they had been using for transactions with me for almost 20 years! They said they could mail me a check. But I was about to go out of town, so that wasn’t going to work. I said they would need to overnight the check to me to make sure it got to me on time and they said they would do this at no charge just this once. Meanwhile, they would also mail me the forms I needed to authorize my bank account. I asked for a supervisor but was not allowed to talk to one. I wrote an angry letter to the president of the company, but have heard nothing back. Vanguard is now in my doghouse.

Weeks later I still didn’t have Vanguard hooked up with my bank yet, so I decided that once I got access I would move some money from my Vanguard Roth IRA account to my Fidelity Roth IRA account. Fidelity’s funds have outperformed Vanguard’s index funds for years, so it was something I was thinking about anyway, but now I had a point to make. I also found out that if you transfer money to your Fidelity Roth IRA, they will give you a match of “up to 10%” of your future Roth IRA contributions for three years. “Up to 10%” required a transfer of $500,000. I’m not sure how someone even gets that much money in an IRA since you can only contribute about $5,000 a year. For lower contributions, the percentage went down. For the $10,000 I was thinking about transferring, the match is only 1%, and not on the $10,000, but on the upcoming contribution which would be $6,500. So $65. But it’s free money.

At Fidelity you can do an asset transfer to pull money from another company’s account into a Fidelity account. You have to have to provide the account number, do a request, and upload a statement from the other company. So I requested they liquidate $10,000 of my Vanguard index fund and move that to my Fidelity account. I wanted this to go pretty quickly because the market can take a jump of a percent or two on any given day and I didn’t want to miss that. One of the things Vanguard teaches is to stay invested because an entire year of gains can happen on only a handful of the biggest gaining days of the year and all the rest of the year is just ups and downs.

Several days later, I found out my transfer request at Fidelity had been cancelled and I needed to call them. They didn’t email me with this information, I am just obsessive and was checking the status of the transfer every day. The asset transfer people at Fidelity work bankers hours so I could only call them during work, which is irritating. Also their telephone system requires you to enter your account number and password over the phone, but their website doesn’t work through the firewall at work, so I had to remember the account number. Anyway, they said because I had a brokerage account at Vanguard they didn’t want to liquidate any assets there. The problem is with a brokerage account I could have some outstanding order on those shares. So they said I needed to liquidate the shares first and re-request the transfer. If the account hadn’t been converted to a brokerage account I would never have had this whole problem. Yet again I was having a hard time seeing how converting the account was making things easier. I thought I might transfer another $10,000 when this was done.

So I did that when I got home that day. Instead of requesting the transfer from the index fund, I sold $10,000 of the fund and requested the transfer from the money market fund that serves as a cash account in the Roth IRA. And I wait a few days, hoping the market wouldn’t get a Santa Clause rally now that it is December. Watching the transfer status, after a week or so, it has been cancelled and I need to call Fidelity (they never tell me this by email).

This time they said Vanguard denied the transfer request and that I had used the wrong account number. I said I had used the correct account number as shown on the statement that I uploaded to them and they said I should contact Vanguard. I called Vanguard and they said they had no problem doing transfers and I needed to get with Fidelity. They offered to set up a 3-way call with Fidelity so we could figure it out. During that conversation I asked if it would be a problem that I was listed as Edward at Vanguard and Ted at Fidelity. Oh yeah, that would do it! They couldn’t possibly transfer between accounts with different names. I said really they are the same name and that I had transferred money between the two accounts before in 2008. They said I could fill out a “one and the same” form at Fidelity, get a medallion signature confirmation (like a notary, but where the guarantor confirms your identity, and apparently not easy to get anyone to do) and mail that in. Ugh. I asked if there an easier way. And they said I could fill out some other Fidelity form and fax it back to them and they would take that. I asked Vanguard if they would be okay with that and they said if it has both names on it and is signed under both names they were fine with it. So I did that. A few days later my transfer request was again cancelled.

The form that Fidelity had said was fine and that Vanguard had said they would accept was not acceptable to Fidelity. I called Fidelity and asked now what? They said I could do the one and the same form. I said what if I just change the name on the Fidelity account to Edward. They said that would work, but I would need to send in a form with a medallion signature and a copy of my birth certificate (which I don’t have and would have to order from Fulton County for $25). I said, you know when I signed up for the account I didn’t have to do all of that, you just took my word for what my name was. They said I guess we trusted you to tell the truth. And I guess now that I’ve been their customer for 20 years, they don’t trust me from some guy they just met on the internet. Eventually they said why don’t you just go to a local Fidelity branch, bring your driver’s license, and they can verify that Edward is my name. So one lunch hour I took the train up to Buckhead and walked a few blocks to the Fidelity branch, filled in the form and they didn’t even ask for my driver’s license. They said they would forward the request to the home office and it would take about a week to see the name change on the account. It’s well into January at this point and I’ve been trying to get this done for a month now with my shares liquidated most of that time. Happily for me, the stock market is doing terribly all this time so I haven’t lost anything by having the money in cash. Eventually the name change showed up, so I requested the transfer again. Do you know what happened? A few days later I checked on the status and the transfer had been cancelled and I needed to contact Fidelity.

I called Fidelity and actually got someone smart this time. He said that I had entered Vanguard as the company I was transferring from, but I should have entered Vanguard Brokerage which is a totally different thing. Switching to the brokerage account was a simplification that just kept giving and giving. And I had entered the money market account and I should have just said to get the money out of cash. Well at least it was a plan and it was easy. So I did the transfer request again. And about four days later the money transferred from Vanguard to Fidelity. The market was crashing badly, so I figured I would only put $5,000 into Contrafund and hold the other $5,000 in cash to see how things go. In the meantime, if I had left the money in the index fund at Vanguard, it would have been worth $800 less. So all that frustration and extra work had at least made me $800. I had inadvertently shorted the market and come out ahead.

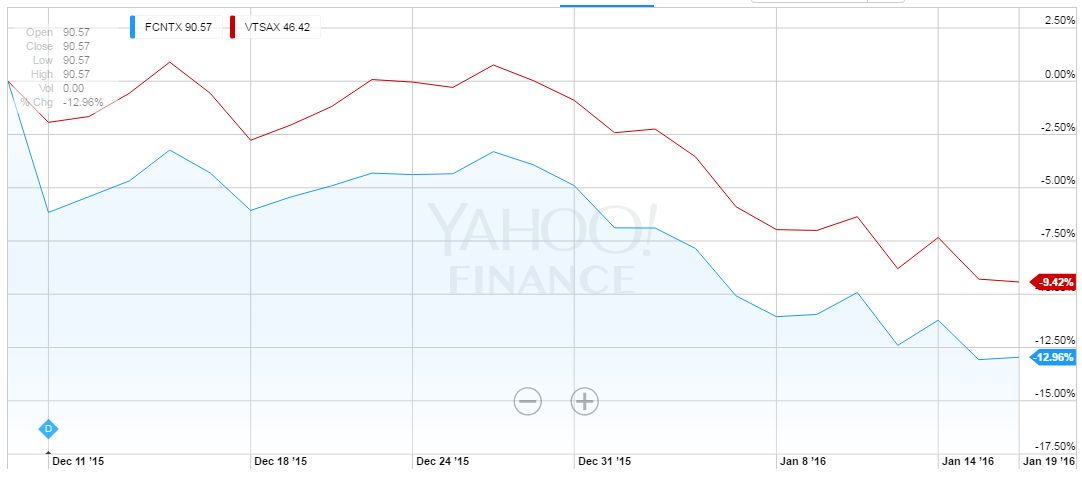

The chart above shows that Vanguard (the red line) lost 9.56% after I sold it (though 0.57% of the “loss” was actually a dividend) while Contrafund (the blue line) lost 12.96% during the period (though 9.05% of the loss was a dividend).

I’ve enjoyed the customer service at Vanguard, but I’ve learned through several conversations they have some really old disconnected systems that cause all kinds of back end manual rekeying of stuff. Maybe that’s how they keep costs down. Green screens. Ironically, they were probably trying to modernize your accounts and broke old stuff that was working fine.

I think the people that run the brokerage are just a whole different crew (maybe a completely independent company) and it is not run as well as Vanguard. I would rather have kept separate accounts to get some benefit from dealing with the real Vanguard.

After two months, a Vanguard rep called me today to talk to me about the letter I wrote to the CEO in December. She said she has avoided changing her account over. I said if the insiders knew not to do this, why was it rolled out as a great solution for the customers? She said her situation is different from mine because she doesn’t use the brokerage. She did apologize and seemed to understand my concerns, but it didn’t sound like they were doing anything about it. They’re still in my doghouse, but I doubt I will close my account.